Iran War = no food?

The Iran war has stopped not just oil flowing, but fertilizer too

Most people, when they think about the consequences of war in the Middle East, picture oil prices. Maybe shipping routes. They don’t think about fertilizer. Unfortunately fertilizer is very affected, and if critical planting windows are missed, the would could be staring down the barrel of a gigantic global food crisis in 12 months.

The strait that feeds the world

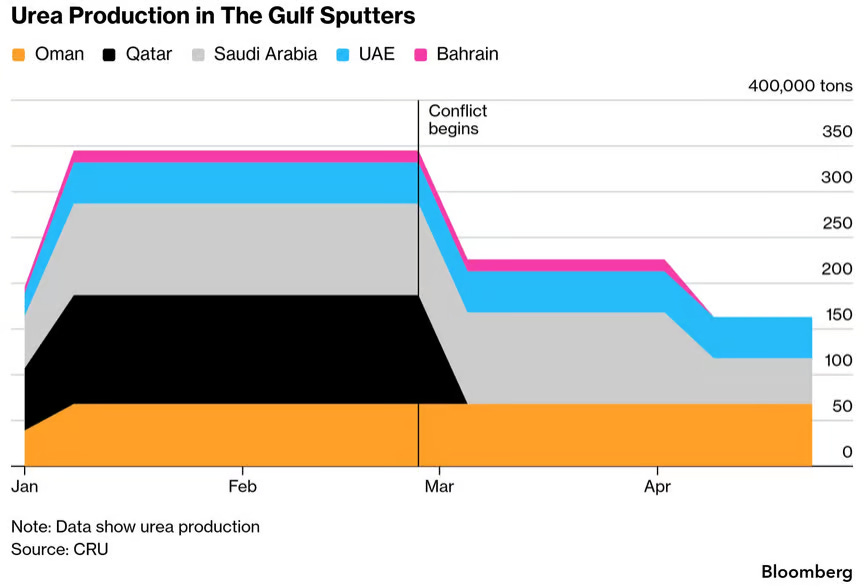

The Strait of Hormuz is famous as the chokepoint for roughly a fifth of the world’s oil. Less well known: it’s also the exit ramp for a massive chunk of the planet’s fertilizer supply. The Gulf states — Saudi Arabia, Qatar, the UAE — are among the world’s dominant producers of urea, a nitrogen-based fertilizer that farmers apply every single growing season to feed their crops. No urea, no crop yield.

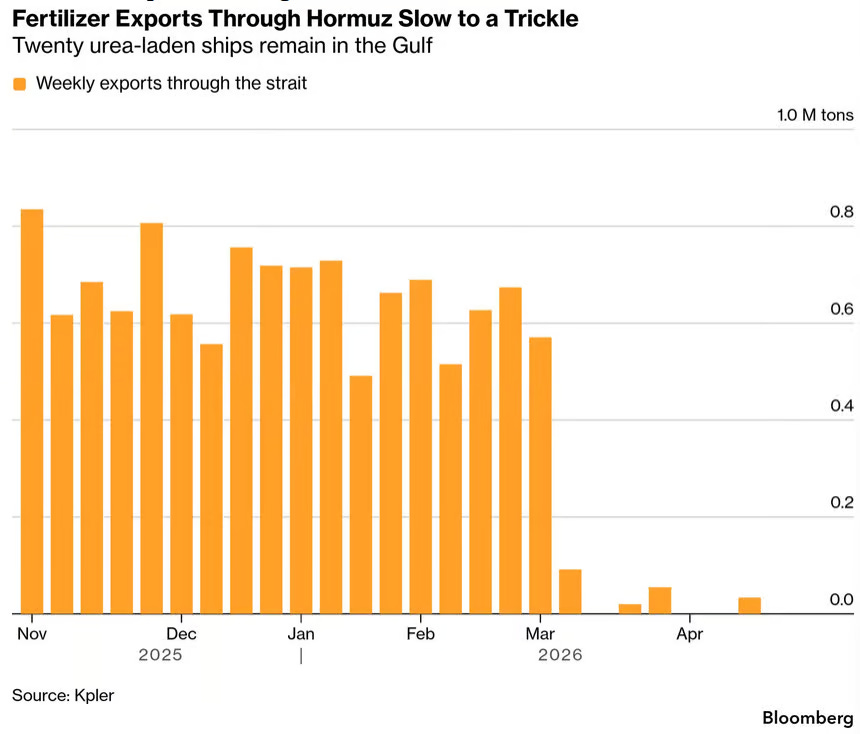

Since the Iran conflict escalated, traffic through the Strait has ground to near-standstill. The consequences for fertilizer flows have been severe. Gulf urea output has collapsed — down more than half compared to pre-war levels — sitting at roughly 160,000 tonnes per week, the lowest point recorded this year. Only 11 fertilizer vessels have successfully made it through the Strait since the conflict began. Meanwhile, 44 ships remain trapped inside the Gulf, most of them loaded and waiting. They can’t leave. Empty ships can’t get in to replace them.

Here’s what makes this worse: producers are now running out of places to store product they can’t ship. When that happens — when warehouses fill and ships can’t move — manufacturers face a binary choice: dump product, or shut down production entirely. We are approaching that threshold.

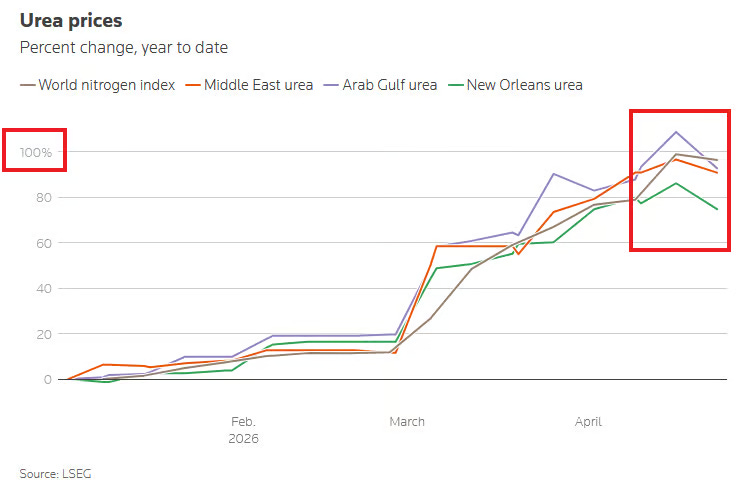

The Middle East supplies roughly 45% of all globally traded urea — feeding major importers including India, Europe, and Brazil. This isn’t a regional problem. It’s a global one.

India just blinked

India is the world’s largest rice producer. It feeds over a billion people. Last month, it placed what was reportedly a record single import tender for urea — and paid nearly double what it was paying just two months earlier. When India panics and overpays, that’s not routine procurement. That’s a country looking at its planting season and deciding it cannot afford to gamble.

The painful irony is timing. Back in 2022, when fertilizer prices also spiked dramatically, global grain prices were near record highs — farmers could absorb the blow because their crops were worth more. Today, wheat and soy prices sit roughly 50% below those 2022 peaks. Farmers are being asked to pay twice as much for fertilizer to grow crops that fetch half the price. The economics simply don’t work.

America’s fields are already failing

Set the Middle East aside for a moment and look at what’s happening in US wheat country. It’s bad independently of the fertilizer story — and together, the two make for an uncomfortable outlook.

Severe drought has locked in across the US Plains. US wheat futures have spiked to around $6.58 per bushel, the highest since mid-2024, and they’re up roughly 30% since January. Only 30% of the US wheat crop is currently rated good or excellent by the USDA — a shockingly low figure. The rest ranges from mediocre to outright failing. Drought stress is accelerating the crop’s development cycle in ways that typically shrink final yields.

And then there’s the acreage number that really stopped me: US farmers are expected to plant the smallest wheat area since 1919. Not since the 1980s farm crisis. Not since the 2008 financial crash. Since 1919. The cost of fertiliser, seed, and equipment has simply made wheat too risky to grow at scale.

Bloomberg’s agricultural commodities index has hit its highest point since late 2023, up 13% over just the past three months. US wheat is up 30% year-to-date. These aren’t warning signs — they’re early effects.

What does this look like in 12 months?

The lag between fertilizer prices and food prices is real and measurable — typically 6 to 18 months. What farmers are deciding right now, about what to plant and how much fertilizer to apply, determines what ends up in supermarkets next year.

If urea prices stay elevated — and there’s no obvious reason they’ll collapse while the Strait remains functionally closed — farmers in multiple major producing regions will apply less of it. Less fertilizer means lower yields per hectare. Lower yields on reduced planted area (see: Western Australia, already pulling back wheat acreage by 14%) means meaningfully smaller harvests. Smaller harvests with static or growing global demand means higher food prices.

The countries most exposed aren’t wealthy Western ones — it’s the import-dependent nations across South Asia, East Africa, and Southeast Asia where food represents 40–60% of household spending. For those populations, a 20–30% spike in staple food prices isn’t inconvenient. It’s a humanitarian event.

For us in New Zealand and Australia, it probably looks more like stubbornly elevated grocery costs, margin pressure on farmers, and a second wave of food inflation that catches policymakers off guard — particularly because most inflation models don’t have a great track record anticipating agricultural supply shocks of this nature.

Why isn’t the world talking about this?

I think there are a few reasons this story isn’t cutting through. Fertilizer is invisible — it’s not a commodity most people interact with. The mechanism is indirect and slow (war → port closure → fertilizer shortage → planting decisions → harvest shortfall → supermarket prices), which means it doesn’t generate the immediate visceral reaction that a fuel price spike does. And frankly, the news cycle is saturated with the conflict itself, leaving little bandwidth for second-order analysis.

But the data doesn’t care about the news cycle. Prices are already moving. Planting decisions are already being made — or avoided. The harvest those decisions produce will arrive in 2027, and by then it’ll be too late to course-correct.

If the Iran conflict can’t be de-escalated in the very near future, then we could be looking at a global scale humanitarian food crisis next year.

Hard to feel hopeful reading this, but that's probably the point. Thank you for the depth of analysis and laying it out clearly.